The goal of maclogp is to compute measures of uncertainty for a model selection method based on an information criterion. Two measures were proposed by Liu, et.al. The first measure is a kind of model confidence set that measures the variation of model selection, called MAC. The second measure focuses on error of model selection, called LogP. Another similar model confidence set adapted from Bayesian Model Averaging can also be computed using this package.

You can install the released version of maclogp from github with:

devtools::install_github("YuanyuanLi96/maclogp")This is a basic example which shows you how to solve a common problem:

library(maclogp)

set.seed(0)

n= 100

B=100

p=5

x = matrix(rnorm(n*p, mean=0, sd=1), n, p)

true_b = c(1:3, rep(0,p-3))

y = x%*% true_b+rnorm(n)

alpha=c(0.1,0.05,0.01)

data=list(x=x,y=y)

models=Models_gen(1:p)

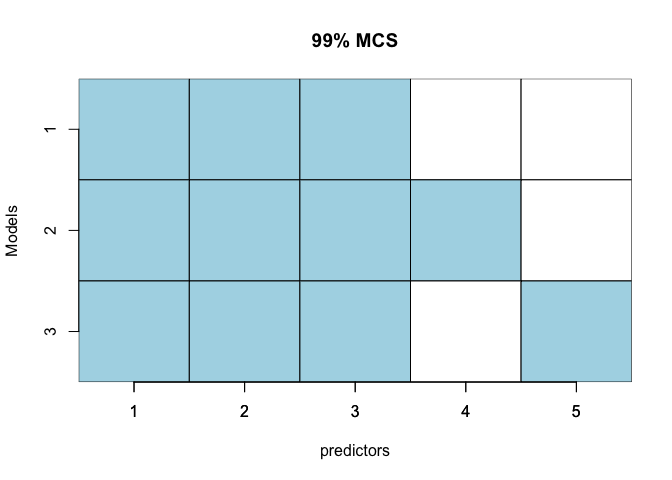

result=MAC(models, data, B, alpha)#default selection criterion is "BIC".

plot_MAC(models, alpha, result$con_sets, p)

#> [[1]]

#> [,1] [,2] [,3] [,4] [,5]

#> [1,] TRUE TRUE TRUE FALSE FALSE

#>

#> [[2]]

#> [,1] [,2] [,3] [,4] [,5]

#> [1,] TRUE TRUE TRUE FALSE FALSE

#> [2,] TRUE TRUE TRUE TRUE FALSE

#>

#> [[3]]

#> [,1] [,2] [,3] [,4] [,5]

#> [1,] TRUE TRUE TRUE FALSE FALSE

#> [2,] TRUE TRUE TRUE TRUE FALSE

#> [3,] TRUE TRUE TRUE FALSE TRUE## References Liu, X., Li, Y. & Jiang, J. Simple measures of uncertainty for model selection. TEST (2020). https://doi.org/10.1007/s11749-020-00737-9.

Need a high-speed mirror for your open-source project?

Contact our mirror admin team at info@clientvps.com.

This archive is provided as a free public service to the community.

Proudly supported by infrastructure from VPSPulse , RxServers , BuyNumber , UnitVPS , OffshoreName and secure payment technology by ArionPay.