![]()

cumulcalib provides non-parametric, tuning-parameter-free assessment of model calibration on the cumulative-sum domain, for two settings:

cumulcalib()

assesses the calibration of predicted risks (Sadatsafavi and Petkau

2024, https://doi.org/10.1002/sim.10138).cumulcalibITE() assesses the moderate calibration of

predicted treatment benefits using data from a randomized trial

(Sadatsafavi et al. 2025, https://doi.org/10.48550/arXiv.2512.08140).The package comes with two tutorials (vignettes), which you can view after installing the package:

vignette("tutorial", package = "cumulcalib") # risk prediction models

vignette("tutorialITE", package = "cumulcalib") # ITE modelsThe package can be installed from CRAN:

install.packages("cumulcalib")You can also install the development version, which includes the individualized treatment effect (ITE) functionality, from GitHub with:

# install.packages("remotes") #this package is necessary to connect to github

remotes::install_github("resplab/cumulcalib")library(cumulcalib)

set.seed(1)

p <- rbeta(1000, 1,5)

y <- rbinom(1000,1,p)

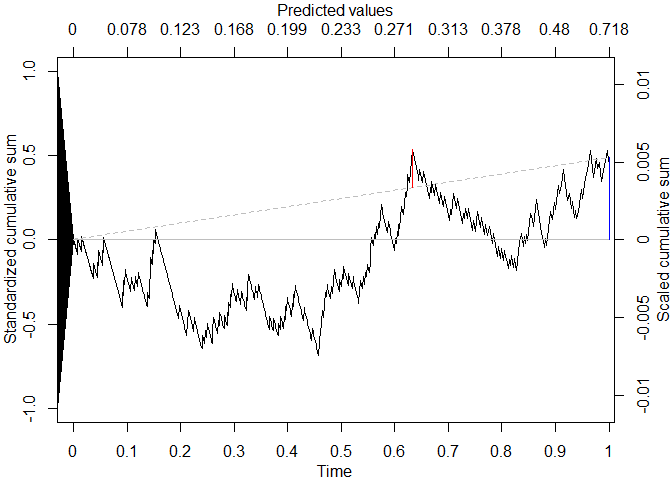

res <- cumulcalib(y, p)

summary(res)

#> Moderate calibration assessment of predicted risks

#> C_n (mean calibration error): 0.00532270104567871

#> C* (maximum cumulative calibration error): 0.00740996981029672 (observed risk < predicted)

#> Location of maximum cumulative error: time = 0.457280572542993, predicted risk = 0.217915058214255

#> Method: Two-part Brownian bridge (BB)

#> S_n (Z score for mean calibration error): 0.489295496431201

#> B* (test statistic for maximum absolute bridged calibration error): 0.904915434767163

#> Component-wise p-values: mean calibration=0.624632509005787 | Distance (bridged)=0.385979705481866

#> Combined p-value (Fisher's method): 0.584068794836004

plot(res)

Need a high-speed mirror for your open-source project?

Contact our mirror admin team at info@clientvps.com.

This archive is provided as a free public service to the community.

Proudly supported by infrastructure from VPSPulse , RxServers , BuyNumber , UnitVPS , OffshoreName and secure payment technology by ArionPay.